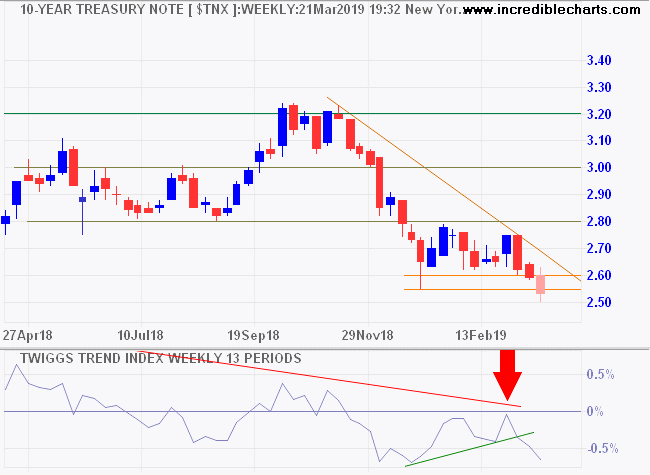

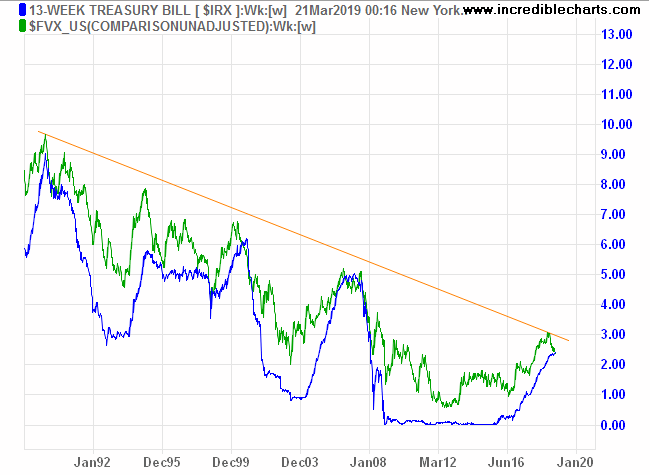

Latest from Colin Twiggs.The Fed did a sharp about-turn on interest rates this week: a majority of FOMC members now expect no rate increases this year. Long-term treasury yields are falling, with the 10-Year breaking support at 2.55/2.60 percent. Expect a test of 2.0%.

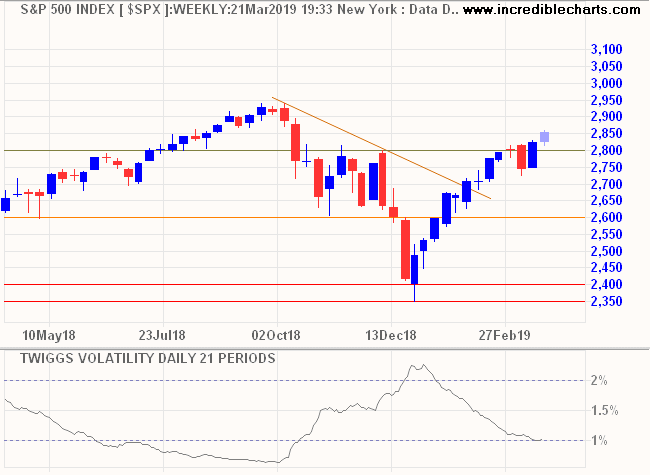

While the initial reaction of stocks was typically bullish, the S&P 500 Volatility Index (21-day) turned up above 1.0%, indicating risk remains elevated.

The reason for the Fed reversal ? anticipated lower growth rates ? is also likely to weigh on the market.

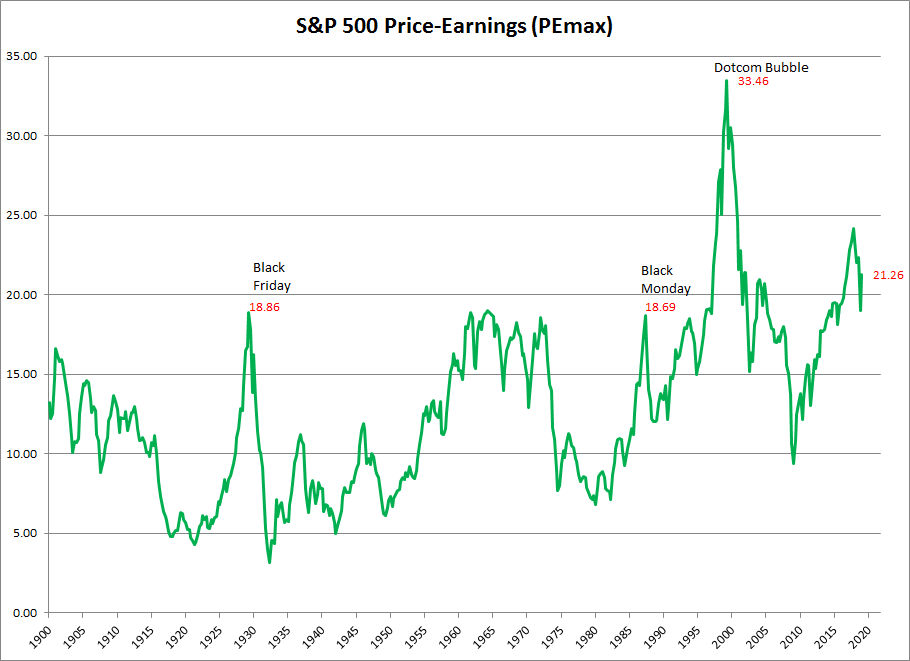

Stocks are already over-priced, with an S&P 500 earnings multiple of 21.26, well above the October 1929 and 1987 peaks. With earnings growth expected to soften, there is little to justify current prices.

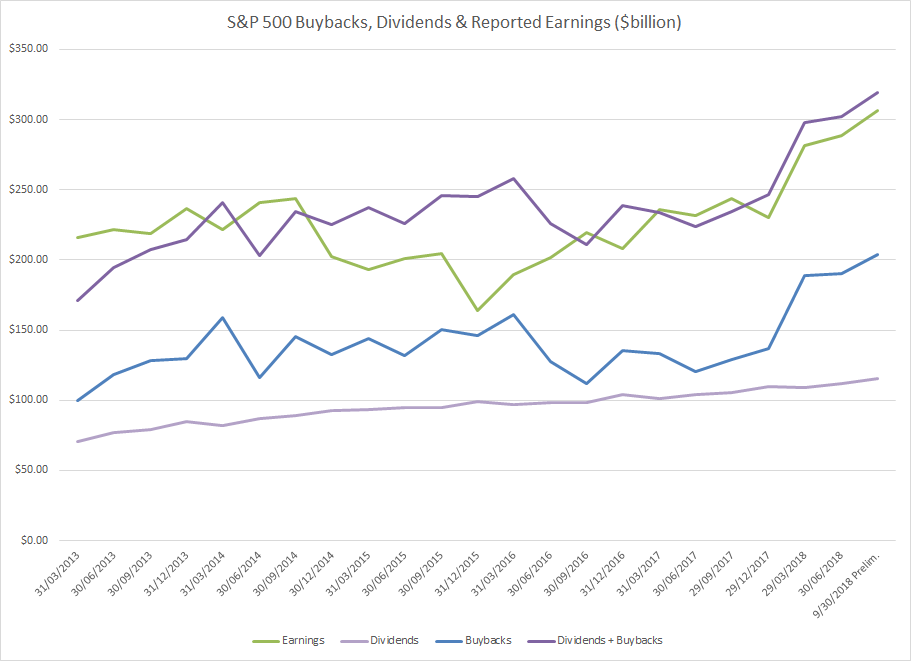

The current rally is largely driven by stock buybacks ($286 billion YTD) which dwarf the paltry inflow from ETF investors into US equities ($18 billion YTD). We are also now entering the 4 to 6-week blackout period, prior to earnings releases, when stock repurchases are expected to dip.

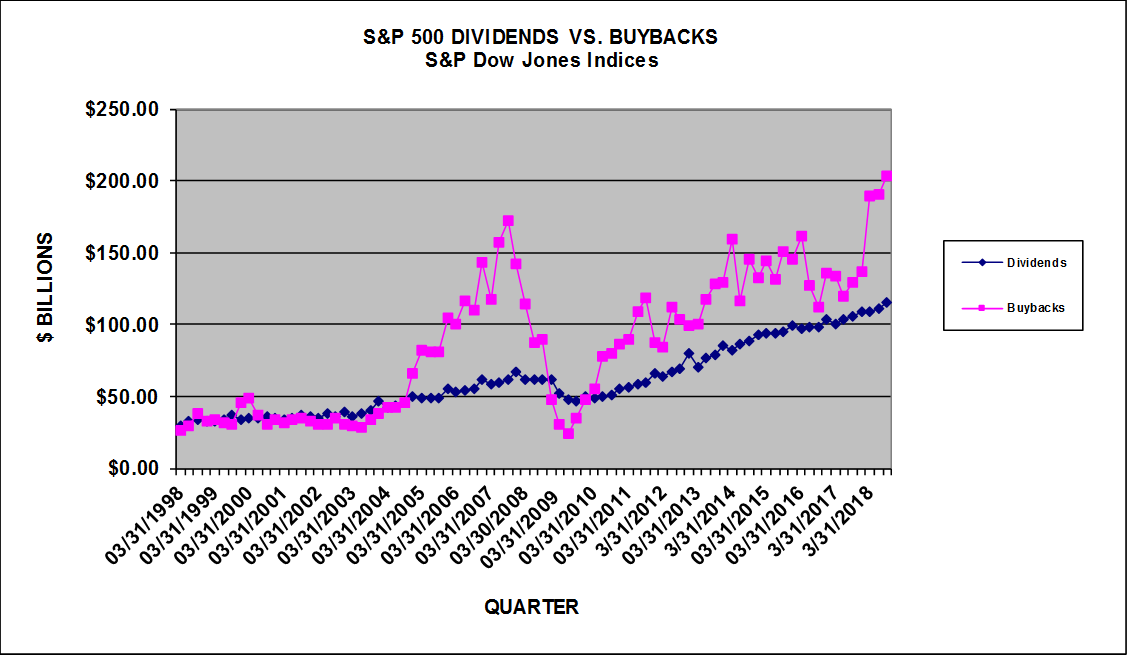

Why do corporations continue to repurchase stock at high prices? Warren Buffett recently reminded investors that buybacks at above a stock's intrinsic (fair) value erode shareholder wealth. If we look at the S&P 500 in the period 2004 to 2008, it is clear that corporations get carried away with stock buybacks during a boom and only cease when the market crashes. They support their stock price in the good times, then abandon it when the market falls.

source: S&P Dow Jones Indices

Shareholders would benefit if corporations did the exact opposite: refrain from buying stock during the boom, when valuations are high, and then pile into the stock when the market crashes and prices are low. Why doesn't that happen?

The culprit is typically low interest rates. It is hard for management to resist when stock returns are more than double the cost of debt. Buybacks are an easy way of boosting stock performance (and executive bonuses).

Corporations are using every available cent to buy back stock. Dividends plus buybacks [purple line below] exceed reported earnings [green] in most quarters over the last five years.

That means that capital expenditure and acquisitions were funded either with new stock issues or, more likely, with debt.

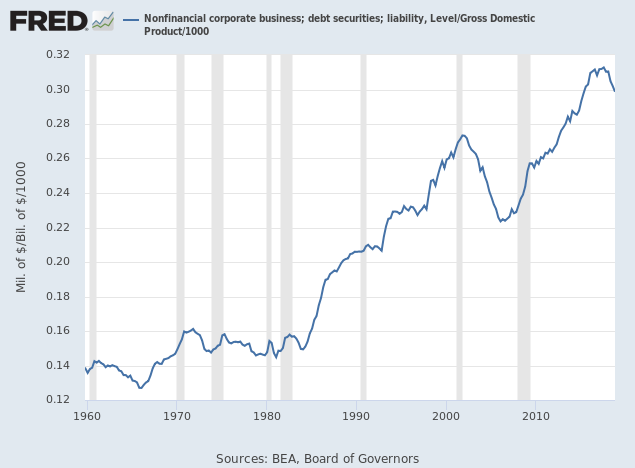

Corporate debt has been growing as a percentage of GDP since the 1980s. The pace of debt growth slowed since 2017 (shown by a down-turn in the debt/GDP ratio) but continues to increase in nominal terms.

Low interest rates mean that stock buybacks are likely to continue ? unless there is a fall in earnings. If earnings fall, buybacks shrink. Declining earnings mean there is less available cash flow to buy back stock and corporations become far more circumspect about using debt.

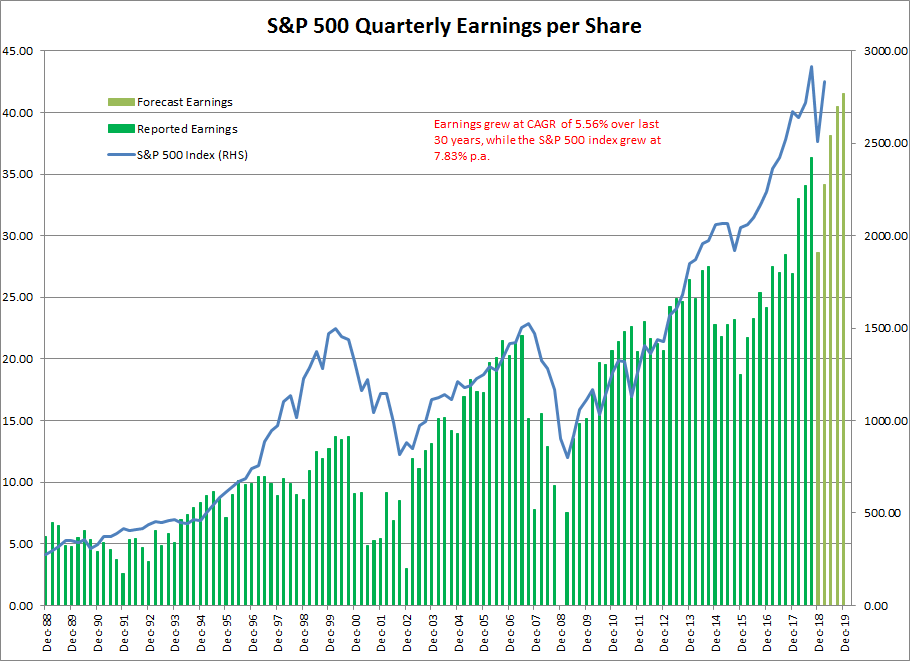

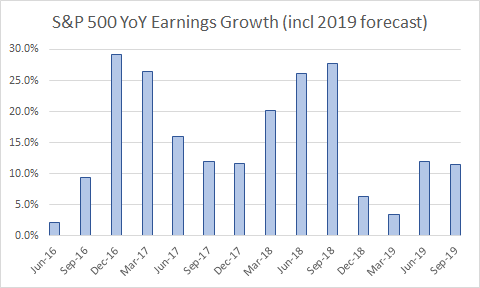

S&P forecasts that earnings will rise through 2019.

But forecasts can change. Expected year-on-year earnings growth for the March 2019 quarter has been revised down to 3.5%. Forecasts for June and September remain at 12.0% and 11.4% (YoY growth) respectively.

If nominal GDP continues to grow at around 5% (5.34% in Q4 2018) and the S&P 500 buyback yield increases to 3.0% (2.93% at Q3 2019 according to Yardeni Research) then earnings growth, by my calculation* should fall to around 8.2%.

*1.05/0.97 -1.

XJO, Gold, MOY and others, page-1252

-

- There are more pages in this discussion • 16 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)