There is a popular but false narrative that the commodity bear market of 2011-2015 was the complete "undoing" of the Commodity Supercycle.

The CRB Index makes it look that way, but it is misleading due to its commodity group weightings and the commodities it leaves out.

Copper and base metals, the heart of the Commodity Supercycle boom, never got anywhere near going back to the price levels of 2002-2003.

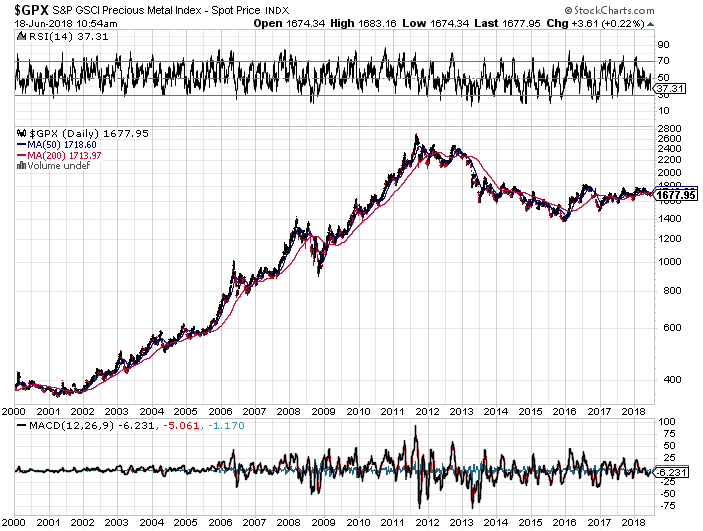

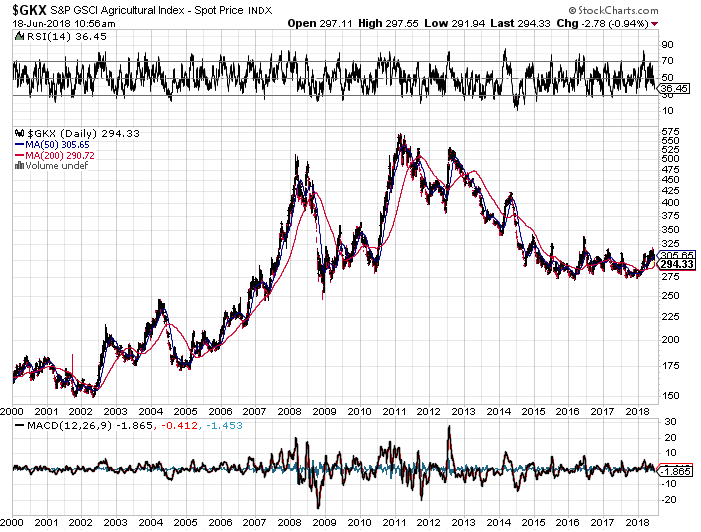

Precious metals and even agricultural commodities and many soft commodities also remain at price levels far above 2002-2003.

Current and future infrastructure projects around the world, including in the U.S. as well as China's Belt & Road Initiative, will drive the next leg up of the Commodity Supercycle, especially in copper and base metals. This idea was discussed in more depth with members of my private investing community, Stock & Gold Market Report.

There is a popular narrative in the markets about the history of the commodity markets (DBC) (GSG) (RJI) (USCI) in recent decades, that goes something like this: Commodity markets boomed as prices soared in the inflation of the 1970s. Then they crashed in the early 1980s, and commodity prices stayed low during the 80s and 90s. (Actually there was a commodity boom in the late 80s, but it didn't get a lot of attention.) Then came the great "Commodity Supercycle" of the 2000s. It collapsed in the 2008 financial crisis, but resumed from 2009-2011. Finally the Commodity Supercycle ended in the bear market of 2011-2015, and commodities have just been recovering from that in recent years.

Like all popular narratives, there are "grains" of truth in the Big Picture story, but it is missing critical details that investors need to understand in order to have the correct analysis and perspective for commodities and commodity stock investments going forward.

Above all, there is this false idea lingering in people's minds that the bear market of 2011-2015 was the complete "undoing" of the Commodity Supercycle before it.

The actual prices and charts show that this is simply not true.

To "undo" a preceding cycle would mean that prices and asset values would go back to where they had been before the previous cycle began. In this case, that means commodity prices circa 2002, before the Commodity Supercycle began. But the prices of copper and other base metals, gold and other precious metals, and even agricultural commodities and many soft commodities have not even gone back anywhere near as low as their old 2002-2003 prices.

Yes, the 2011-2015 bear market represented a major downturn and pullback for these commodity prices - but they have always remained at price levels that are quite elevated on a historical and long-term basis. I dare say I believe that base metals (JJC) (JJCB) (CPER) (CU) (DBB), precious metals (GLD) (PHYS) (GDX) (GDXJ) (GOAU), and possibly grains (JJG) (RJA) (CORN) (WEAT) (SOYB) will never go back to their 2002-2003 price levels ever again - just like prices will never again return to the levels of the 1960s or 1930s.

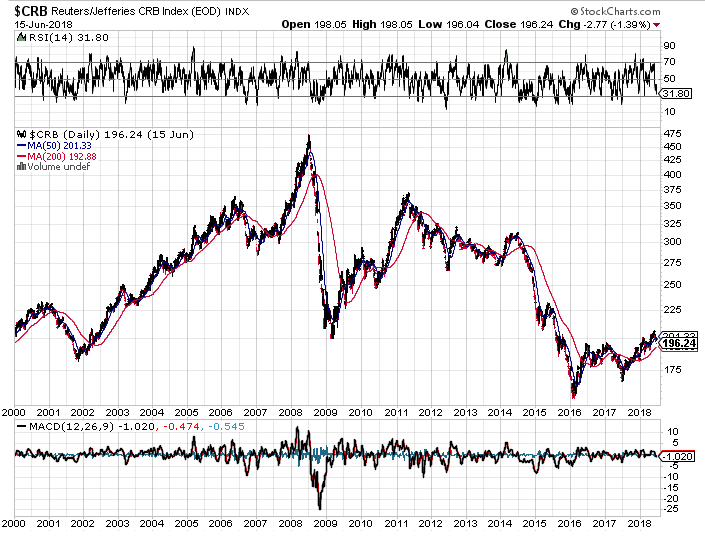

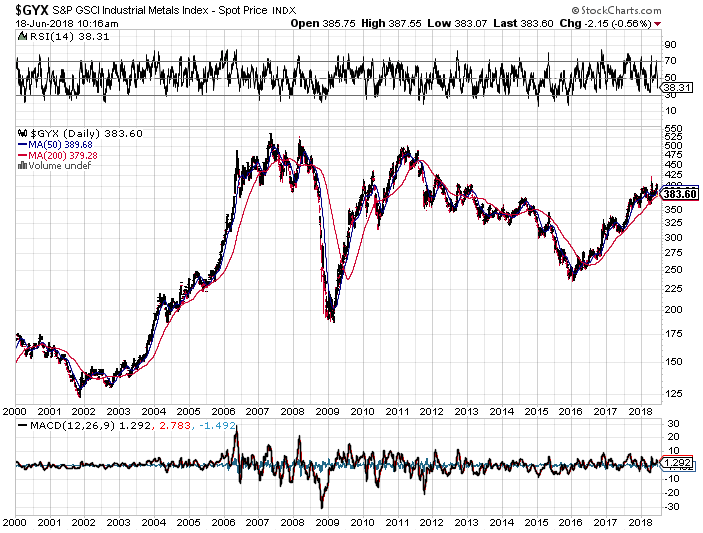

Unfortunately the most well-known and widely-followed broad index of commodity prices, the CRB Index, paints a very misleading picture of overall commodity price performance over the past 15 years. That is because it overweights the significance of oil, gas, and petroleum based commodities, it underweights the significance of base metals and leaves out key base metals entirely, and it contains a large and random collection of soft commodities.

So let's compare and contrast the price charts of the past two decades for the CRB Index ($CRB) vs. the Industrial Metals Index ($GYX):

You can see that these two charts really reflect two very different long-term trend dynamics over the past two decades. The CRB Index in early 2016 crashed all the way down below its 2001-2002 low level, and it is just now recovering to 2002 levels. The Industrial Metals Index on the other hand, which tracks the prices of copper, aluminum, nickel, zinc, and lead, even at its early 2016 low remained far, far above its 2001-2002 low level, and even above the temporary low in the 2008-2009 crash.

The conclusion is that base metal prices have permanently reset themselves on a higher level that was established during the great Commodity Supercycle.

I argue that the "Commodity Supercycle" has a lot more to do with industrial and base metals in particular, since the trend was driven predominantly by China's massive consumption of industrial raw materials in its construction and infrastructure building boom of the 2000s.

Different commodity groups have very different dynamics, and they may not always follow the same trends. Even when they go in the same direction, they may move at very different rates, and their starting and ending price points may be dramatically different from each other, as the two charts above show clearly.

The CRB Index lumps together an assortment of selected commodities from each of the various groups, and gives them certain weightings that may or may not reflect their actual significance. I consider this a poor way to measure and analyze trends in the commodity markets.

For example, in the CRB Index petroleum based products "based on their importance to global trade, always make up 33% of the weightings". Oil really is its own market, with its own dynamics distinct from any other commodities. This is true even more so for natural gas.

The CRB Index, which tracks a total of 19 commodities, only includes 3 base metals: copper, aluminum, and nickel. While these are all important, including aluminum and nickel, while leaving out zinc and lead, distorted and diluted the impact of base metal prices on the CRB since the year 2000. The charts below show how the long-term price trends of aluminum and nickel lagged far behind zinc and lead for most of the last two decades: Furthermore, the CRB Index includes many so-called "soft commodities": cocoa, coffee, cotton, orange juice, and sugar. Like natural gas, each of these commodities are really distinct and unique markets, often with little correlation to each other or to any other commodities. Trading Places was a great movie, but I wouldn't make long-term investment decisions involving fundamental global economic trends and industrial commodity consumption based on orange juice futures.

Meanwhile, the trends in more significant markets like precious metals and agricultural grains have also shown a reset to a much higher level, even after the recent bear market, far above the pre-Commodity Supercycle prices:

The bottom line is this: Copper, other base metals, and iron ore are the true heart at the core of the Commodity Supercycle boom.

The boom was driven predominantly by China's voracious consumption of industrial raw materials in its construction and infrastructure building boom of the 2000s. Above all, this required massive amounts of copper, steel, iron ore, zinc, lead, and nickel. Most people in the market think the Commodity Supercycle ended with the bear market of 2011-2015. I disagree. I think the supercycle merely got put on pause for a few years. And I think it "unpaused" in 2016: the copper and base metal rally we have seen in the past couple years, is the first step in the resumption of the Commodity Supercycle.

To be sure, investors and traders who made the unfortunate mistake of buying these commodities or the stocks of the companies who mine them in 2011 or 2012, suffered heavy losses from 2011 to 2015. To them, such losses surely felt like the end of the supercycle.

But from a global economic perspective, I think the picture looks quite different. China's industrial activity didn't grind to a halt in 2011-2015. Technically it didn't even slow down, it just stopped growing at an increasing rate the way it had in the decade of the 2000s.

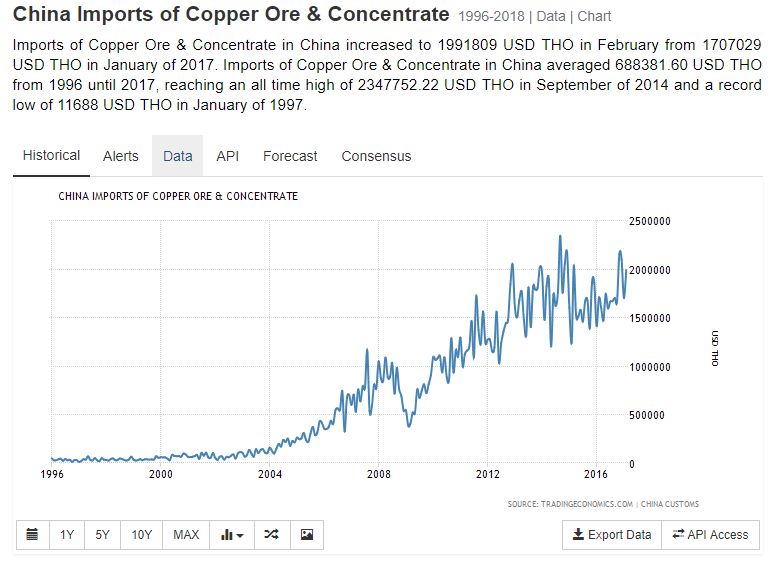

Consider this article published by Mining.com on June 8: "Copper price: Chinese concentrate imports hit 18-year high". Yes that's right, the article spells it out:

The demand for copper concentrate is surging. Concentrate cargoes landing at Chinese ports increased 37% from May 2017 to total 1.58m tonnes in January.

Concentrate imports for January to May now total 7.8 million tonnes, the highest for the period since at least 2000.

Yes, China is importing more copper right now than it was during the peak of the Commodity Supercycle!

Here is a chart of China's imports of copper ore & concentrate from 1996 to the present:

Does this chart look like the Commodity Supercycle is ending? No, it certainly does not!

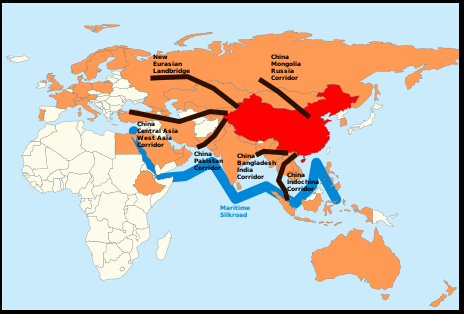

Meanwhile, China is proceeding with its massive "Belt & Road Initiative", whereby they are building large-scale infrastructure and transportation projects across all of Asia and into Europe, the Middle East, and Africa:

Of course China is doing this to improve its own trade routes with all of these regions, as it competes with other countries to increase its share of global trade. But in the course of building the infrastructure projects themselves, they will have to purchase and consume massive amounts of iron ore, copper, and other base metals.

At the same time, the rest of the world, including the United States, will also have to undertake a large amount of work to rebuild, expand, and modernize our infrastructure. This is something that Trump and Republicans and Democrats alike would have to agree on. They may have different plans for it, they may go about it in different ways, but somehow or other they all realize that crumbling and inadequate infrastructure has to be rebuilt, expanded, and modernized. And whichever way they end up doing it, it will surely require an awful lot of copper, steel, iron ore, and other base metals as raw materials.

I haven't even talked about the much greater amounts of copper wire required in electric vehicles and all electrical equipment and items. Then there is the battery market, which drives demand not only for lithium and cobalt, but also for good old-fashioned nickel as well.

AML Price at posting:

32.0¢ Sentiment: Buy Disclosure: Held

Furthermore, the CRB Index includes many so-called "soft commodities": cocoa, coffee, cotton, orange juice, and sugar. Like natural gas, each of these commodities are really distinct and unique markets, often with little correlation to each other or to any other commodities. Trading Places was a great movie, but I wouldn't make long-term investment decisions involving fundamental global economic trends and industrial commodity consumption based on orange juice futures.

(20min delay)

(20min delay)