just found this one from LRS's FB, worth reading, FYI

Lithium Investing: Asia Makes Bold Investments To Secure Supply

Feb. 5, 2018 3:41 PM Summary

Chinese battery manufacturing capacity continues to attract capital as the nation significantly increases electric vehicle production.

The country is nearly entirely dependent on the foreign produced energy metals such as lithium and cobalt.

Junior exploration companies operating in South America have already attracted significant capital to advance near-term projects; An acquisition of an advanced junior lithium has taken place.

Why I believe Chinese material and investment companies will continue to want to secure supply and the impact this will have on advanced junior lithium companies.

Over the past few years, demand for lithium batteries has skyrocketed due to the mass global adoption of consumer electronics such as smart phones, laptops, and tablets. The total impact on the lithium supply chain has been minimal as each device contains only a small amount of raw materials like lithium and cobalt. Now, larger consumer applications, such as electric vehicles and home battery storage systems, are transitioning to lithium batteries and away from traditional lead-acid batteries. These new applications for lithium batteries command a significant amount of lithium per unit compared to consumer, handheld, electronic devices. For example, on a lithium carbonate equivalent basis, a mobile phone contains 1.7g, a tablet contains 20g, and a pure electric vehicle contains 19,000g.

As these new applications take flight, demand for lithium will continue to rise at a much more rapid rate due to the increases in the quantity demanded per unit. This new demand will put pressure and create opportunities within the lithium supply chain to deliver meaningful new supply. As illustrated throughout this document, the strategic Chinese battery and investment companies alike have already begun to acquire and invest directly into advanced exploration companies. It is in my opinion that based on these underlying themes, the valuations of select junior lithium exploration companies could see their stock price appreciate over the next few years and even be subject to additional acquisition activity within the space. Due to these macroeconomic trends, I remain bullish on the near and mid term valuation of advanced lithium junior exploration companies and fully expect that strategic Asian companies to bring additional new investment capital to the industry in 2018 and 2019 along with off-take agreements. This will continue to be one of the key themes in the lithium exploration and mining industry over the next 2 years.

It has become clear that the increase in demand will be driven through applications that consume a large amount of raw material per unit. The use of lithium batteries in stationary energy storage systems has become increasingly popular, especially since pricing has come down from around$1,000kWh to the $200-300kWh range. With billions of dollars being invested in global battery manufacturing capacity, especially in China, there are few reasons why pricing will not break through the $100kWh barrier. This will allow for a greater number of stationary storage systems to be sold in new markets, such as in residential properties. The North American average residential energy storage system contains 14kWh of storage capacity while utility-scale projects have installed upwards of 100MWh of capacity.

In the early 1990s, Japan-based Sony Corp (NYSE:SNE) released the first consumer lithium battery, which was initially integrated into a line of video recorders. Flash forward 25 years: the Japanese and Koreans are fighting to maintain their leadership position in the research, development, and production of lithium batteries. The Chinese have also recently emerged as a potential leader in the battery space. The primary driver for the Chinese to invest in the business is to shift their automobile industry to a new, cleaner energy form, such as battery technologies. This shift is being propelled by the need to control emissions and smog within city centers throughout the nation. In 2017, the Chinese government mandated that all automakers producing over 30,000 vehicles per year must produce 10% of its capacity in the form of electric drive or purchase credits from another automaker. Both domestic and foreign automakers have raced to announce various line-ups that will be made available in 2019-2020 as they do not want to be at a disadvantage in the largest global marketplace for automobiles.

In the past year, the supply of strategic metals, such as lithium, has been placed under the microscope as Asia moves to significantly increase battery manufacturing capacity. Today, lithium is produced in Australia, Chile, and Argentina and then sent to conversion or processing plants located inside or outside of China. To assist with meeting increasing lithium demand, Australian lithium hard-rock mining companies are now shipping unprocessed material directly to Chinese processing facilities, something that I view as a desperate move by Australia as it truly eliminates any value add. This low value business practice is being accepted due to the shortage in global lithium supply but this model also assumes that China has established the necessary processing facilities and technical know-how. This will become a limiting factor when discussing the amount of unprocessed hard-rock materials Australia exports to China.

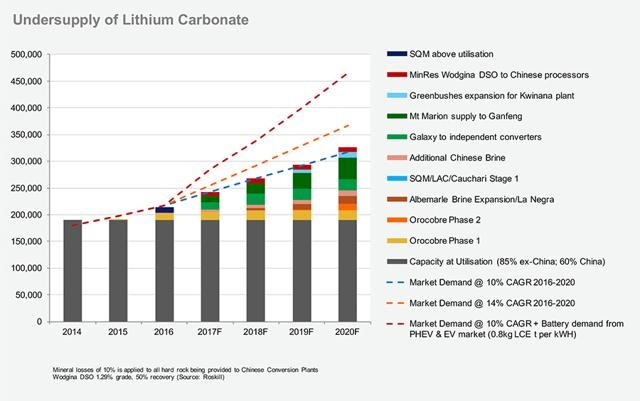

As illustrated in the “Undersupply of Lithium Carbonate” graph, new supply over the next few years will be primarily recognized from expansions at existing facilities and projects that are at an advanced stage, such as Lithium Americas’ Cauchari project. Based on the information presented, there are at least three new sources of hard-rock material being sent to Chinese or independent converters and processors. This will likely become the short-term solution for new lithium supply, which is less than ideal due to both chemical grades and the high cost associated with hard-rock mining compared to lithium salars. In the lithium brine space, the industry is expecting Albemarle (NYSE:ALB) and Orocobre (OTC:OTCPK:OROCF) to expand existing facilities in South America while limited Chinese brine capacity is introduced before the end of the decade. Despite the new supply entering the market, on a base case scenario, the industry will continue to be in an undersupply situation until 2021-2022. Looking at the most bullish scenario, which assumes a higher level of electric vehicles being adopted, then there will be a fundamental shortage of raw materials in the marketplace.

Prior to 2025, some new brine facilities in Argentina will be brought to market while existing producers will likely have completed another phase of facility expansion. Conclusively, no Asian countries are actively producing any significant amounts of lithium carbonate with only a small amount of lithium production coming from China over the next several years. Many industry observers still have great levels of doubt that the Chinese will be able to produce any meaningful volumes of battery-grade lithium brine from their salars.

Asian investment, mining, and battery manufacturers are now looking outward to invest and acquirecompanies that allow them to achieve security in long-term lithium supply. Simply stated, these large Chinese organizations know that lithium demand has now become fundamental to their automotive industry so, to ensure success in their primary business, they need to secure a long-term supply of lithium and other metals. For Asian companies, this is exceptionally difficult as there are only a handful of lithium producers that are not presently owned by the Chinese and these are all multi-national blue-chip companies. Thus, the Asian investment capital has moved further upstream into the lithium exploration market. In 2017, the industry witnessed a number of Chinese investments with a primary focus on Argentina. Here is an overview of several investments the Chinese completed in the past year into the lithium exploration and production market:

NextView – Chinese investment company NextView completed the acquisition Toyota Tsusho (OTC:OTCPK:TYHOF) – Through a Joint Venture with Australia-based Orocobre (OTC:OTCPK:OROCF), the company is looking to expand the output at the flagship lithium brine asset, Olaroz. The Joint Venture has been ramping up production at Olaroz over the past two years and is now in a position to expand production from 17,500 T LCE per year to 42,000 T LCE, at a capital cost of $160 million. Final details Chemphys – The battery material company that specializes in the production of high grade lithium carbonate and battery-grade lithium hydroxide made a direct investment through a private placement into junior lithium explorer NRG Metals (OTC:OTCQB:NRGMF). The private placement was valued at $1.4 million and is being used as exploration capital. Despite NRG Metals being at a very early stage in the exploration cycle, Chemphys has expressed its intention to purchase all lithium materials produced by NRG. NRG is working on two projects in the Lithium Triangle with the most significant development being the"Homebre Muerto North Project" or HMNP. HMNP is located in the Salta and Catamarca Province comprising a total property package of over 3,000 hectares, encompassing six concessions. The company has reported good surface sample collections, magnesium to lithium ratios, and is located across from Galaxy Resources’ Sal de Vida lithium development project.

Ganfeng – Established in 2000, the Ganfeng Group is the largest integrated lithium producer in China, with a total annual capacity of 30,000 T LCE. Ganfeng's products include lithium metal, lithium hydroxide, lithium carbonate, lithium fluoride, and lithium chloride. In the past year, Ganfeng has moved to cement a position in the Lithium Triangle through a strategic investment in Lithium Americas (OTC:LACDF). Over the past several years, Lithium Americas has been developing its world-class lithium brine asset at the Cauchari basin. The financial agreement saw Ganfeng invest $190 million in consideration for 19% of Lithium Americas. A private placement was completed for $50 million and $125 million was issued for project debt. This capital is allowing the company to move forward with its construction plans. Meaningful volume will be delivered in 2020. Ganfeng has also secured an off-take agreement for Lithium Americas’ lithium production from the Cauchari project.

Visiting Lithium America’s site in Argentina – November 2017

Golden Concord Group – Through the investment subsidiary Million Surge, a private placement was completed with Millennial Lithium for $30 million. GCG is best known as the world’s largest manufacturer of high quality photovoltaic materials. The funds will be used to advance Millennial’s (OTC:OTCQB:MLNLF) flagship lithium brine asset, Pastos Grandes.

Asia is not limiting its interest to lithium supply, it is also targeting other strategic resources such as cobalt. Automotive-grade batteries generally contain cobalt, making the energy metal a critical component to the lithium battery supply chain. It has become well-known that cobalt is primarily extracted from Congo as the largest proven reserve can be found there. In addition to mining cobalt, it is a by-product of copper and zinc. Ningbo Shanshan, a large Chinese lithium battery anode materials company, invested$265 million into China Molybdenum, a major global energy metals miner that is ranked as the second largest cobalt manufacturer in the world. To ensure that the company has good exposure to existing and developing mining districts, the funds are being deployed to expand its position in both Brazil and Congo. This clearly illustrates that the Chinese are expanding investments across the entire energy metal industry.

Photo of Ganfeng Lithium Facility in Jiangxi Province, China

The underlying theme is that Asia is very serious about building an industry on lithium batteries, but is entirely dependent on importing strategic metals. As battery manufacturers continue to build out manufacturing capacity, the amount of Asian investment throughout the supply chain will continue to deepen. It is my expectation that late-stage junior lithium exploration companies will continue to attract investment from strategic Asian partners. The acquisition of Lithium X by NextView indicates that Asian companies are willing to acquire full projects rather than invest through share ownership. It is in my opinion that the lithium industry will continue to see a growing number of Asian companies that will commit to off-take agreements and participate in financing rounds with junior explorers in Argentina.

It is in my opinion that other junior lithium exploration brine companies operating in Argentina could become potential takeover targets. It is also clear to see that the junior market can attract capital from various Chinese firms, regardless of whether it is a $1 million or $30 million placement, or a major financing such as was seen by Ganfeng into Lithium Americas. The other key takeaway is that investment is flowing from various Chinese sectors, including: battery and solar material companies, trading firms, and investment companies. Although the industry is very mature, new supply is required to meet emerging applications, such as electric vehicles, so 2018 will continue to see additional investment from China into South America and other promising regions of the world. It is still unclear how many other Chinese investment companies are well capitalized and searching for low cost lithium assets. Due to the rising cost of lithium, it is expected that battery material firms will search out investment opportunities to ensure that they are well positioned and have raw material for their production facilities.

All of the information presented revolves around investments made by Asian companies, not factoring in any moves from American or European investment, automotive, or material companies to secure supply. Should the Western world wake up to the reality that they want a serious position in the lithium production market, then they will need to move in the near future. The general rule is that the best projects attract capital first, meaning that the Asian companies are acquiring positions within the best companies and projects. In theory, if the Western world wants a position in the market then this scenario could increase the value of lithium assets around the world, especially for lithium juniors looking to develop low cost brine assets.

Author's note: If you enjoyed this article than be sure to receive future material by clicking on the "Follow" tab at the top of this page or on my profile. Disclosure: I am/we are long AVLIF, OROCF.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

LRS Price at posting:

1.1¢ Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)