Contrarian, long/short equity, Deep Value

MARKETPLACE

Unorthodox Mining Investing

(2,805 followers) Summary

In Q3 2018, Alacer Gold will start producing gold from the sulfide zone of the Copler mine.

In my opinion, there are two not widely known factors that have a positive impact on the company's valuation.

In this article, I discuss these factors; in the final section, I am trying to assess the updated value of Alacer shares.

This idea was discussed in more depth with members of my private investing community, Unorthodox Mining Investing.

I am a big fan of under-followed, unpopular precious metals mining companies. Alacer Gold (OTCPK:ALIAF) is such a company. It currently runs the Copler mine, an open pit oxide ore operation located in east-central Turkey. Very soon, in Q3 2018, the company plans to commence mining at the sulfide zone of the Copler deposit. In my opinion, this project has a big, positive impact on the company's valuation. According to the technical report for the sulfide expansion project, its net present value is $728M. However, there are two issues not widely perceived:

Due to the fact that the project is 85% completed and most of the capital expenditures have been already made, the project's value is much higher than that disclosed in the economic study.

Over the years, the company has stockpiled a lot of sulfide ore, improving the project's economics further.

As a result, today, the company's shares are undervalued, and Alacer presents, in my opinion, an interesting buying opportunity. Introduction

As I have mentioned above, now Alacer is at the final stage of construction of the so-called "sulfide expansion project". Shortly speaking, in 2011, the company started mining operations at the oxide zone of the Copler mine in Turkey. Then, in 2016, Alacer commenced construction of the sulfide expansion project at this deposit. Now the construction is 85% completed, and in Q3 2018, the company should pour the first gold coming from the sulfide zone. According to the economic study for the Copler sulfide expansion project (SEDAR, June 9, 2016), the upgraded mine will produce 3.5 million ounces of gold over the next twenty-six years of mining and processing. Sulfide Expansion Project

The project's value

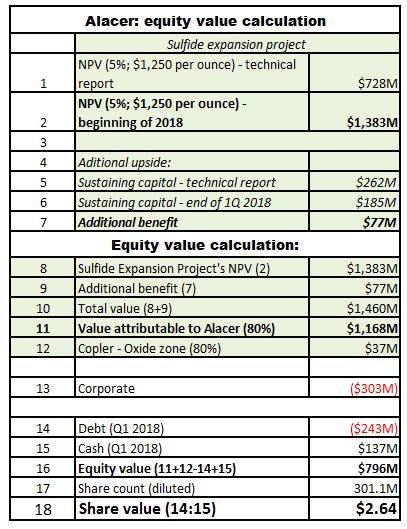

The technical report for the sulfide expansion project (page 354) discloses after-tax free cash flows generated by the project over the life of the mine. The undiscounted value of these cash flows is $1,483M. However, after excluding sunk costs of $570M (capital deployed for the construction in 2016 and 2017), it is very easy to arrive at an updated net present value of the project. According to my own calculations, this value stands at $1,383M (using the price of gold of $1,250 per ounce and a discount rate of 5%).

Additional upside potential

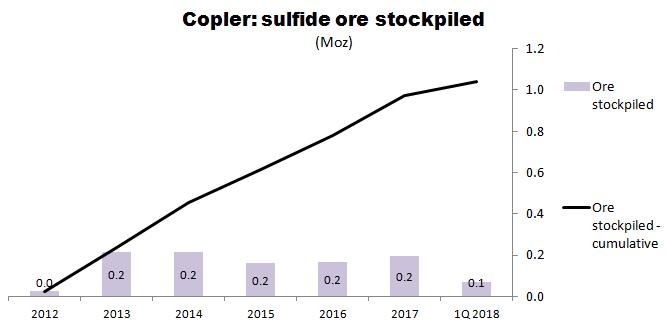

Interestingly, the company started stockpiling the sulfide ore many years before taking a decision to commence construction of the sulfide expansion project. As a result, over the years, it has stockpiled more than 1 million ounces of sulfide material:

Source: Simple Digressions

I guess it is not widely known information. However, in my opinion, the stockpiled sulfide ore offers the additional upside for the project. Why? Simply put, the capital deployed to extract this ore qualifies as a sunk cost and improving the project's economics. In other words, over the life of the mine, the company will show lower sustaining capital spending than initially planned. Here are the appropriate figures. Firstly, look at sustaining capital disclosed in the economic study (the row marked in red):

Source: Alacer

Note that over the life of the mine, the sustaining capital expenditures are estimated at $74 per ounce of gold. Now, according to the mine plan, the sulfide expansion project is supposed to deliver 3,546 thousand ounces of gold. To mine this gold, Alacer is expected to spend sustaining capital of $262M (3,546 thousand x $74 per ounce). However, over the last six years, the company has stockpiled as many as 1.04 million ounces of gold coming from the sulfide part of the mine. As a result, instead of deploying $262M, the company will have to spend only $185M ($77M, i.e. 1.04 million ounces x $74 per ounce, has been already spent).

Value of equity

Finally, here is the table documenting the way I have calculated the project's net present value (the area marked in green) and the value of Alacer's equity:

Source: Simple Digressions Notes:

Row 12 discloses the net present value of the Copler oxide zone attributable to Alacer; it has been calculated using the data disclosed in the technical report for the sulfide expansion project

Alacer holds an 80% stake in the Copler mine (row 11)

Row 13 discloses the net present value of cash outflows related to corporate costs (administrative and exploration expenses); I roughly estimate that Alacer's annual corporate expenses will amount to $20M

As of the end of March 31, 2018, the company held cash of $137M and debt of $243M

The current diluted share count is 301.1 million

As the table shows (row 18), one share of Alacer is worth $2.64. Today, these shares are trading at $1.86, so the company is undervalued. Catalysts

Share prices breakout

Most recently, Alacer shares have broken above their medium-term resistance level (the area marked in orange):

Source: Stockcharts

The chart shows that over the last eleven months, Alacer shares were trading in a wide range (C$1.95-2.40) and a few days ago, they broke above the upper limit of this range. According to technical analysis, any breakout above a medium-term trading range indicates the chances for a new upward trend. If I am correct, a strong move up is likely.

Gediktepe - a possible catalyst

Apart from Copler, the company has a 50% stake in the Gediktepe project located in western Turkey (the remaining 50% is owned by Lidya Mining, a Turkish mining company). It is a relatively small deposit, at least compared to Copler. According to the latest mineral reserve estimate, Gediktepe hosts 24.9 million tons of ore grading, 1.19 grams of gold per ton of ore (or 953 thousand ounces of gold, of which 50% is attributable to Alacer). However, in my opinion, it is too early to present a reliable opinion on this deposit. This year, the company is expected to release a definitive economic study for Gediktepe, so, until then, I would refrain from any comments on this project. Gold prices

The project's net present value was calculated using a price of gold of $1,250 per ounce. Today, gold is trading at around $1,300 per ounce, so the project's value calculated above is underestimated. Risks

Political risk

Turkey is ruled by Recep Erdogan, the current president of the country. I do not want to go deeply into politics, but, generally speaking, Turkey is not perceived as a democratic country now. As a result, investors are advised to check the current political situation. However, in my opinion, the risk is not particularly high. The country is struggling with relatively high unemployment (around 10.6%), so the Copler mine, offering new jobs to the local population, should be perceived as a positive factor for the Turkish economy. Sulfide ore processing

The sulfide ore at Copler is refractory. It means that it is not amenable to standard cyanidation processing. That is why the company has to apply a sophisticated and expensive technology called "pressure oxidation (POX)". Well, I do not want to go very deeply into technical issues but let me say this:

Up to now, Alacer was processing the Copler oxide ore using a standard heap leaching technology. The POX method is a new thing for Alacer and, as such, it may be a challenge. Of course, the company has made necessary tests and hired an experienced project manager (Foster Wheeler) but… bad things happen, particularly when mineral processing is concerned. That is why I am going to monitor the project's performance very closely.

Poor quality of an economic study for the sulfide expansion project

Unfortunately, the quality of the economic study for the sulfide expansion project is pretty poor. For example, the company does not present a detailed cash flow model for the project (production figures, revenue, costs, capital expenditures etc.). Instead of it, there is a table disclosing annual free cash flows to be delivered over the life of the mine. In my opinion, the quality of this material is below the industry standards and any investor interested in putting money into Alacer shares should keep this fact in his/her mind.

Did you like this article? If yes, please, visit my Unorthodox Mining Investing section where I manage a portfolio of up-to-ten mining picks, discuss new investment ideas and provide my subscribers with a medium-term outlook on a few financial markets (particularly the base / precious metals market). Most recently I have introduced a new section called "Developers". This service is dedicated to mining companies planning to open new mines within one or two years. Disclosure: I am/we are long CEF, GDX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

AQG Price at posting:

$2.52 Sentiment: Buy Disclosure: Held