Share

2,083 Posts.

lightbulb Created with Sketch. 32

clock Created with Sketch. 29/05/18

14:27

Share

Originally posted by nocelery

↑

Disclosure: this is my largest holding, so I have a very strong interest in this stock appreciating (further).

Expand

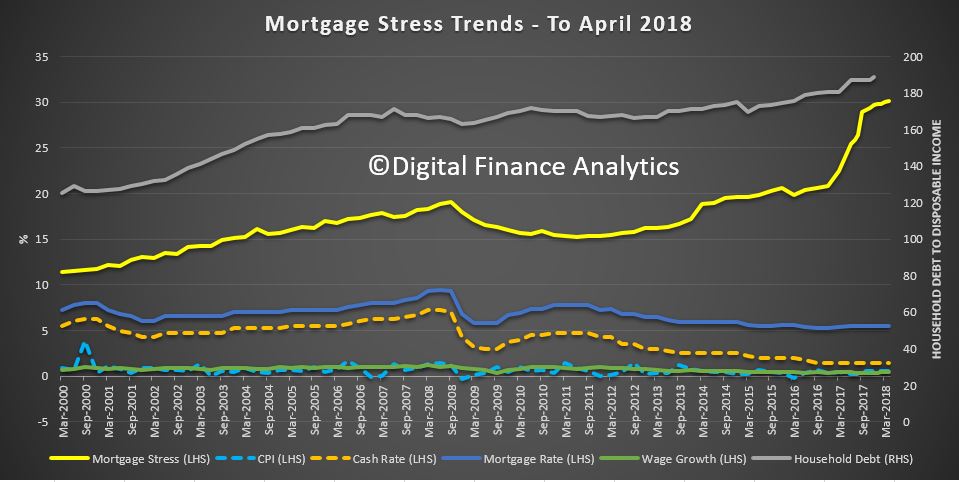

Housing market - With mortgage stress at record highs, what happens to outstanding MNY loans (say car loans) when house prices fall, mortgage repayments rise and/or more people default on their mortgages?