There are costs with shorting but no more than a long position and they can be less. Re time horizon: I thought AGM would be very bearish for WOR and it was with Blackrock exiting at $7.11. But 10 days later buyers poured in and SP has gained $2.40 which has surprised me.

But with WOR... time favours the shorts. Each day there is no ann of contracts means WOR's revenue/earnings continue to decrease .i.e. NO news IS news. If contracts were being announced every 10-14 days as was previously the case, I'd be long gone. But only 2 so far this HY with only 18 work days left indicates situation is poor if not outright bad for WOR. Mr Mkt has bought WOR's thesis that revenue doesn't matter coz 'were're cutting costs and margins will rise'. But revenue does matter. Firm continues to be totally obscure/opaque with shareholders re the outlook statements, which to me indicates seriousness of situation.

So i don't have a fixed time period but at HY in Feb management will be forced to reveal rev/earnings for 1hfy17 and i expect it will be weak indeed. I have a big position in WOR but at $9.51 would add to it if more cash was handy as i feel SP is way overvalued. Hence, i urge holders to grab this price as risk is strongly to the downside imo. Contractors need contracts.

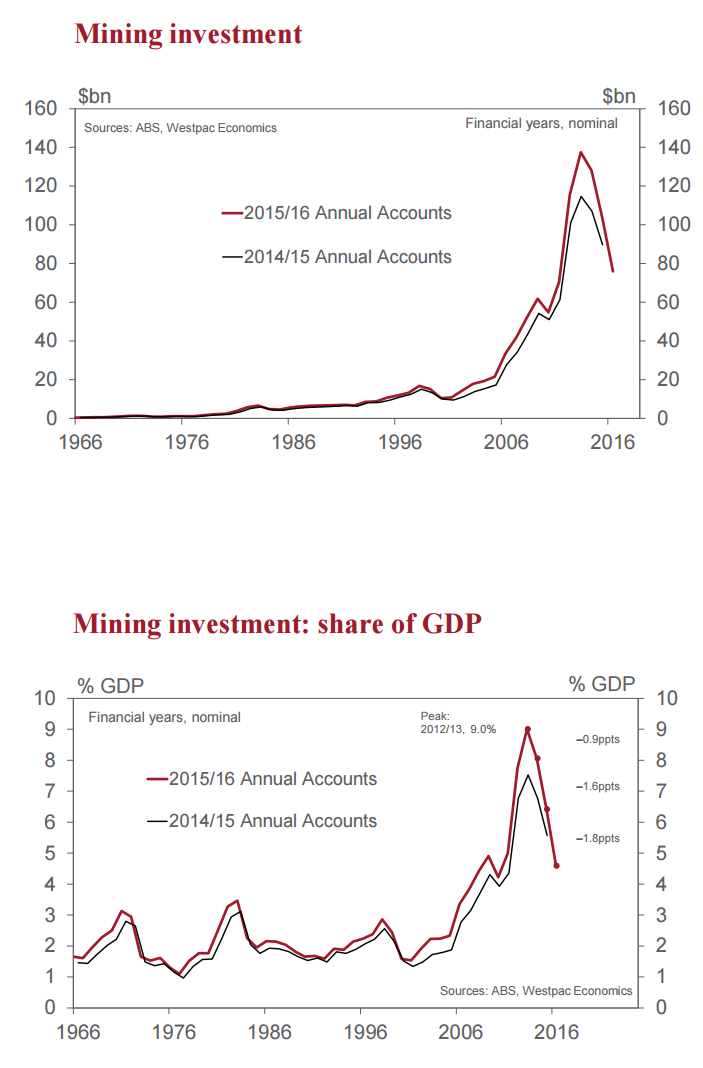

More info out today re mining/energy capex in Oz from Westpac. The figures speak for themselves. Capex worldwide has taken a similar massive hit.

Via Westpac:

• The Annual National Accounts for financial year 2015/16 included revised estimates for business investment. Here we provide a brief recap of recent trends.

• In terms of the mining / non-mining investment picture there are a couple of key take outs.

• The mining investment boom has been revised higher. It appears that some investment previously allocated to other industries has been reclassified.

• Non-mining business investment has a more pronounced cycle over recent years.

Mining investment: The timing of the peak in mining investment remains 2012/13. In nominal dollar terms, mining investment climbed to a high of $137bn, upgraded by almost $23bn from the 2014/15 annual national accounts. As a share of the economy, mining investment peaked at 9.0% in 2012/13, upgraded from 7.5% – a rather sizeable revision. For the 2015/16 financial year as a whole, mining investment moderated to 4.6% of GDP. The end of the mining investment boom is in sight. Work on the remaining gas projects under construction is due to be progressively completed during 2017.

Ann: Qatar Shell Awards EPCM Contract for Pearl GTL, page-30

Add WOR (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

$13.86 |

Change

-0.120(0.86%) |

Mkt cap ! $7.649B | |||

| Open | High | Low | Value | Volume |

| $14.11 | $14.16 | $13.86 | $12.08M | 868.4K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 7 | 13996 | $13.86 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $13.87 | 2900 | 1 |

View Market Depth

| Last trade - 16.10pm 27/11/2024 (20 minute delay) ? |

| WOR (ASX) Chart |